Portfolio performance FY 2025

Compounded Annual Return of 19.76%

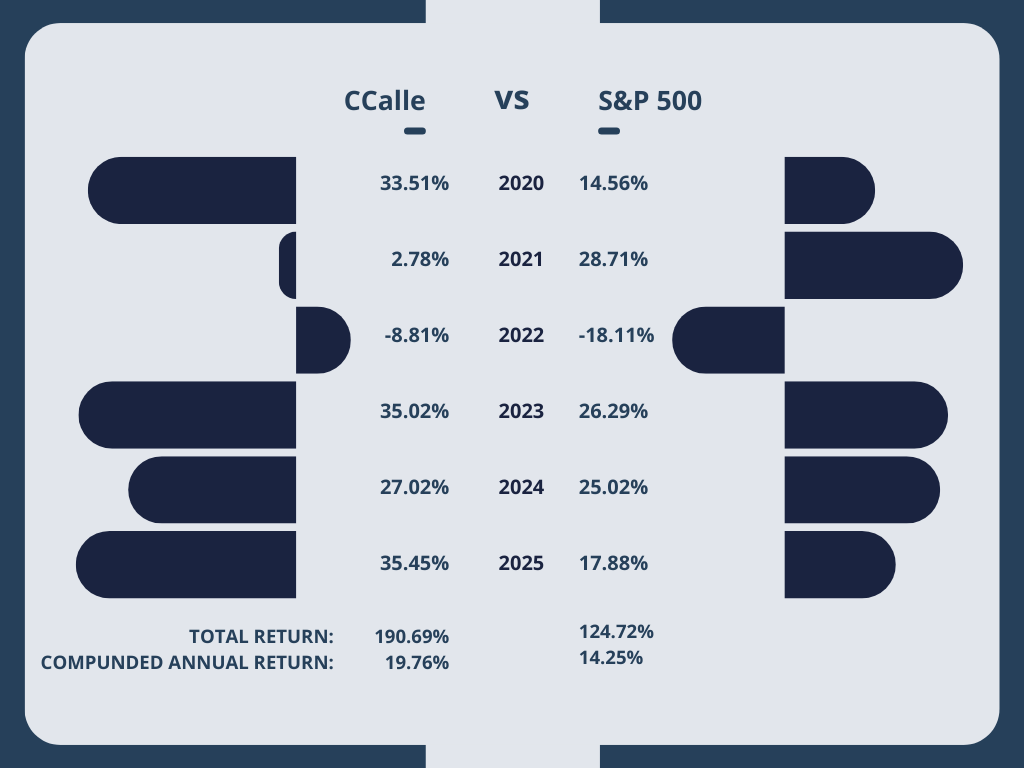

The portfolio has returned 35.45% in 2025, compared with a return of 17.88% of the S&P 500, dividends included. The year 2025 marks the third consecutive year of beating the index, and the fifth out of six since inception.

The total return of the portfolio since inception until December 31st, 2025, is 190.69%, compared with 124.72% of the S&P 500. This makes the compounded annual return of the portfolio sit just below 20%, with 19.76%, compared with 14.25% of the S&P 500.

Risk, Beta, and Alpha:

Risk, beta, and alpha are usually terms that professional investors use to describe how good their returns have been, adjusted by volatility. I never pay attention to beta or alpha, which makes me a big contrarian in the industry. These words don’t come out of a bad year. On the contrary, my Beta in 2025 has been 0.02, which means that my portfolio wasn’t correlated with the index, and my Sharpe Ratio was 1.43 (usually, above 1 is good).

What I pay attention to is the risk that we are assuming in our portfolio, but not from a volatility perspective. Instead, I focus on business criteria: balance sheet risk, earnings risk, and valuation risk.

When I analyze a company, the first step is checking its balance sheet. Even a wonderful business becomes riskier when there is leverage in its balance.

It is actually easy to understand. If you think of a restaurant, you may be interested in buying the best one in your city, which generates a lot of cash for its owner. But if the owner is a fool and obtained more debt for the restaurant than what it can pay down with its earnings, then you probably don’t want that business anymore.

The same happens with earnings. When an industry or a company has record sales, we need to ask ourselves if those earnings are sustainable or just respond to a market trend.

Let’s go back to the restaurant example again. There’s a huge difference between a good restaurant that is always full and a new restaurant that is very trendy now, but will probably fall into oblivion next year. In the market, there are these two types of companies, too. Paradoxically, Mr. Market is usually willing to pay a higher price for the trendy restaurant, since its earnings are booming. There’s always hope that they can keep growing for many years. But that’s also the source of big money losses: fast growers that become a bust.

Hence, we need to differentiate between sustainable earnings, potential sustainable earnings growth, and momentary earnings growth.

In the end, we have the valuation risk. This is probably the easiest to understand, since the price we pay is directly linked to the return we will have. The lower the price, the higher the return. I’m probably not a suspect of avoiding growth at all costs, since I’ve bought companies like Games Workshop, Celsius, or even Wise recently at a high PE ratio. But to pay for growth, I need to be sure that growth will be in the cards for many years. Otherwise, I prefer having the option of growth for free.

Portfolio’s movements:

Sales:

Many people ask me when and for what reasons I sell the companies I hold. It’s completely normal, since many people try to explain when to buy, but not so many explain when to sell. Let me tell you my approach.

First, I differentiate between good businesses and bad businesses. If you were lucky enough to buy a good business at a good price, you probably won’t want to sell it. Never.

But I do.

Bad businesses, though, usually require a very low price and a catalyst on the horizon to own them, since you don’t want to be stuck with a bad business in the portfolio. In the case of bad businesses, when the price reaches my fair value estimate, I’m out. Simple as that, because I don’t want to be an investor in a bad business for too long.

But good businesses… that’s another story. Some, as I said before, never sell them. That’s arguably one of the biggest mistakes Warren Buffett has committed during his investing journey. When he owned Coca-Cola at the end of the 1990s, he didn’t sell, even when the price was ridiculous. Hence, until after 2016, he didn’t recover what he could have made back then (disregarding dividends).

I’m personally not willing to sit for over 16 years to make money. Hence, when the market is willing to overpay for a good business, I’m willing to sell. Of course, I won’t sell it immediately after it reaches my fair value estimate. After all, good businesses always surprise on the upside. But if the market is willing to pay for many years of growth today, I’m out.

Then I come to my sales this year. I only sold three positions in 2025: in February, I sold Google and Rightmove, and in July, I sold Amadeus. I sold these businesses at

GOOGLE: 184.7 dollars per share

RIGHTMOVE: 666.8 pence per share

AMADEUS: 71.02 euros per share

Google finished the year at 313.8 dollars per share, which made me miss a profit of 69.8%. Rightmove finished the year at 519.60 pence per share, which made me miss a loss of 22%; and Amadeus closed 2025 at 62.84 euros per share, which made me miss a loss of 11.5%.

Needless to say, all three of them are still on my radar, but I’ll only buy them back if the price is attractive.

At this point, I want to reflect about missing profits when selling good businesses. Yes, that’s a risk. And every strategy has its own risks. For me, it is clear that I won’t buy the next big thing, since it will seem expensive to me. I will also miss the supposed next big thing that finally goes bust. The trade-off is worth it for me, since I not only chase performance, but also capital protection.

I’ll also miss when great businesses become highly appreciated by the market. It has happened in the past, with companies like TransDigm, Google, Meta, and many others. And it will keep happening in the future. That’s never been an issue in obtaining a good performance, though.

The trade-off here is also worth it for me. I won’t participate in market exuberance, probably missing some profits. But I won’t participate in the disillusionment part when everyone is disappointed with some business, sending its valuation to low PE ratios. I may miss some profits sometimes, but I will certainly miss the losses, too.

Purchases:

There’s little difference between my portfolio at the end of 2025 and the beginning of the year. Of course, the three companies I sold are not part of the portfolio anymore. The new companies in the portfolio are: Fortinet, LVMH, and Bank of Georgia.

Fortinet finished the year with an allocation of 1.46% of the portfolio, LVMH with 2.22%, and BGEO with 6.21%, after a spectacular return since I purchased it.

But the most important change during the year has been the increase in the weight of Argan SA. You can read my thesis here. Argan finished the year with a weight of 14.03%, from 2.78% at the end of 2024. This increase in weight answers mainly to two factors: Argan is widely undervalued, offering safety for our investment, and it also offers a high dividend yield, which rewards us while we wait for its value to be recognized by the market. In a market where growth has a high price, and speculation drives prices, finding businesses with these two characteristics is like finding an oasis in a desert: strange and rewarding.

The market, overall:

People focus too much on the market as a whole. I prefer a bottom-up research, focusing on a company’s strengths and weaknesses. There is no point, in my opinion, in debating about the economy as a whole if you want to invest in individual businesses.

Still, it makes the headlines. And money managers tend to feel forced to talk about the economy, even if it adds little value. Especially, I would say, when they have a bad year.

This said, I do think that the US market is expensive. Lately, I’ve seen people adjusting the price of the index for the quality of the businesses, or even discounting several years of growth. But the truth is that when you need to adjust too much to justify a price, you’re probably overpaying.

Will the market fall like a rock? Who knows. But I do know that I want exposure to good businesses at reasonable prices, and not to good businesses at too high prices. Otherwise, I may finish needing to wait for a decade to recover what I once had.

Last words:

To finish this brief recap, I want to thank all copiers of my portfolio for their trust. To me, it is a blessing that more than 2,000 want to invest exactly like I do. Thank you.

Next month will be my 72nd month investing publicly on eToro, and I will share more thoughts about these 6 years of investments. Remember that you can still follow me on eToro.

Yours sincerely,

Cristià Calle Mercado.