Important Red Flags People Might Be Missing About Microsoft

A contratian view of Microsoft's Investment Thesis

Microsoft released results, and everyone is excited about them and for a good reason, since revenue growth and earnings are quite good. But have you seen the red flags? Let’s dive into them.

But first, these are the quarterly results:

Revenue increased by 18% to $76.4 billion in Q4 2025

Operating income grew by 23%, to $34.3 billion

Net income increased 24% to $27.2 billion

Diluted earnings per share increased by 24%, to $3.65

The red flags:

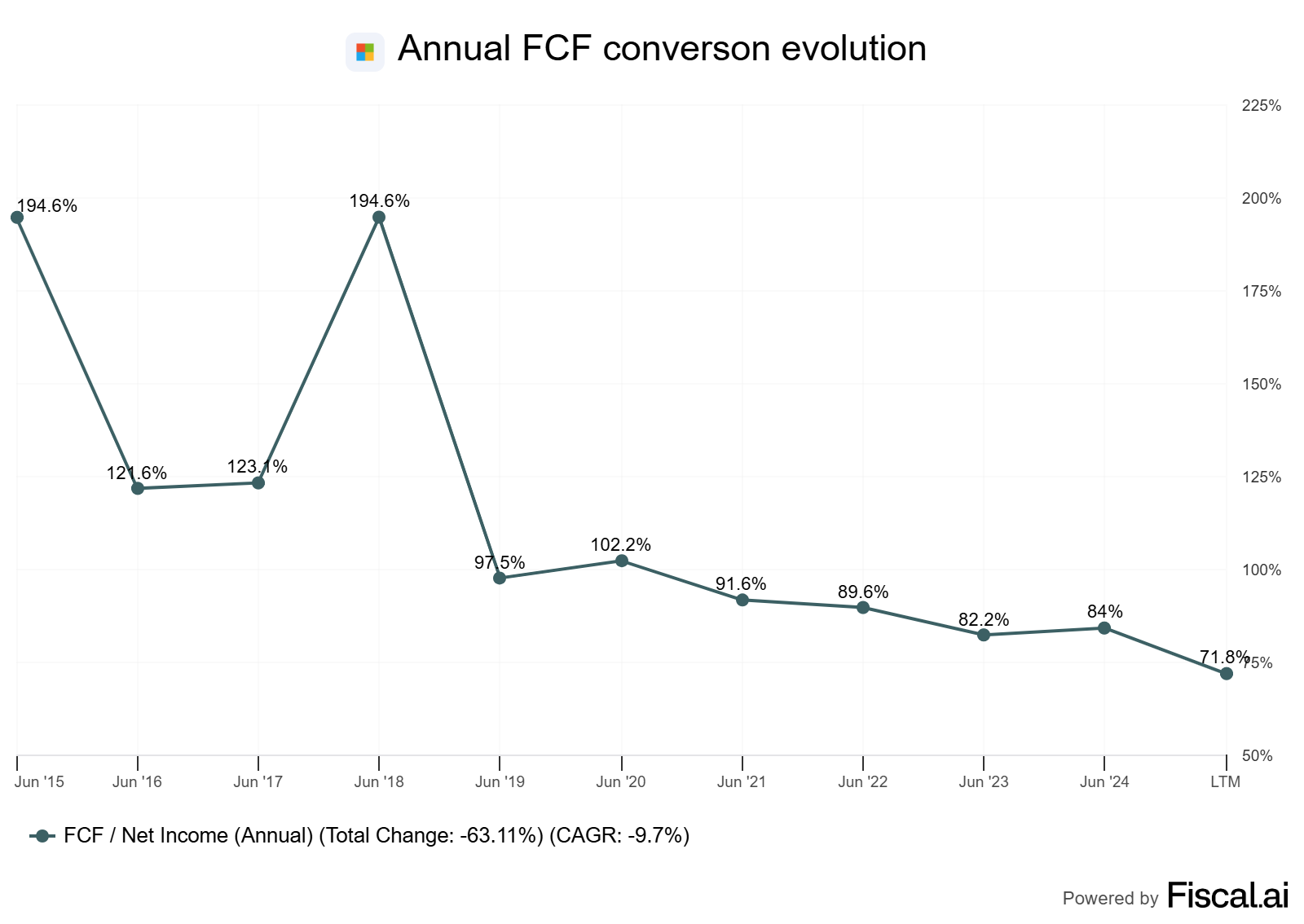

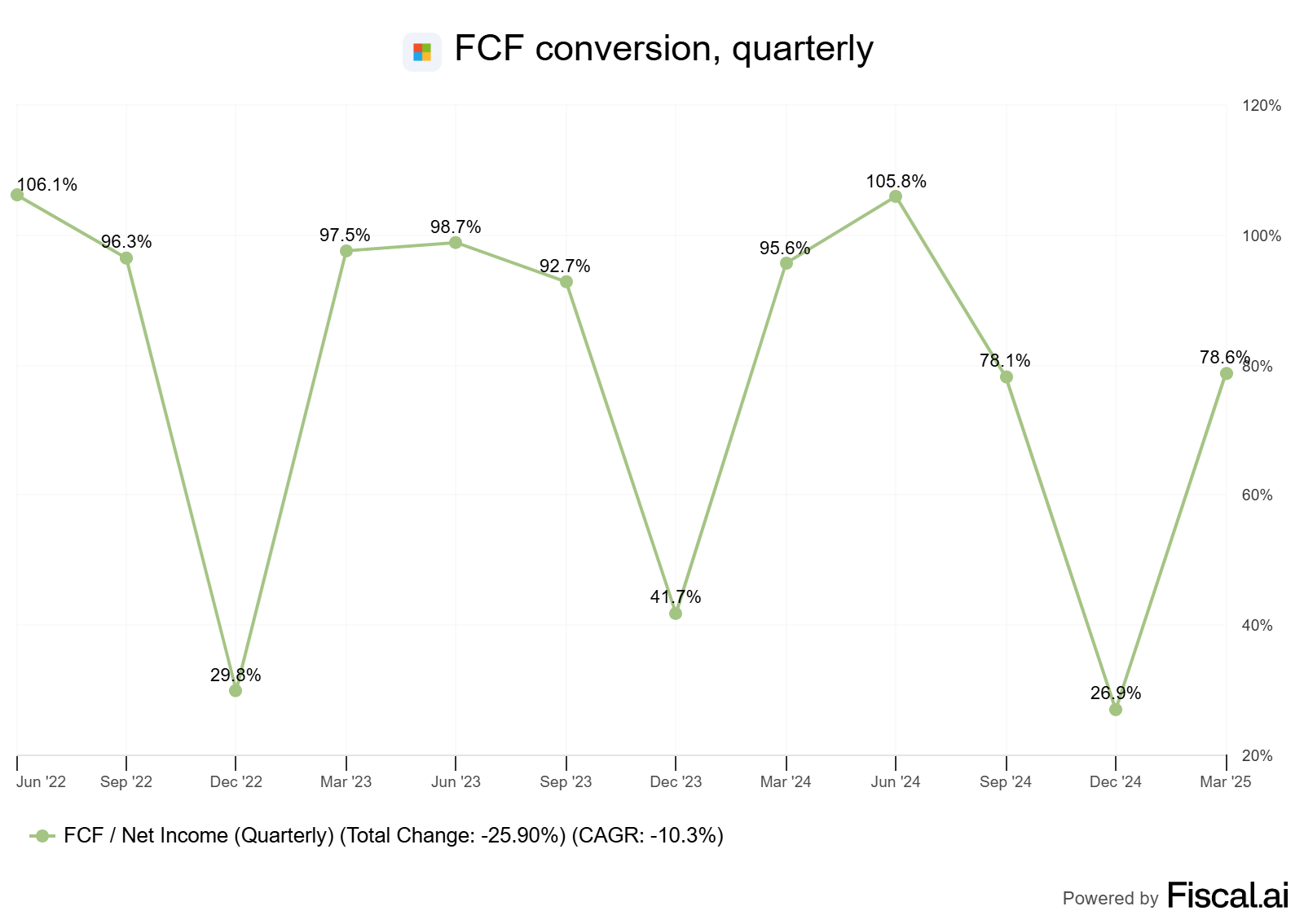

Free cash flow conversion:

FCF conversion has historically been high for the company. In fact, it has consistently been above 100%, since the company has been collecting money in advance, increasing the “unearned income” of the company consistently. However, since June 2021, the company’s CAPEX has been eating into the company’s free cash flow.

This has historically been seen as a sign of reinvestment into the business and its growth, but it is a red flag to be aware of. In the end, what we as investors will get is the cash that the company generates.

A possible terrible consequence for the company’s future free cash flow is a stagnation of growth while CAPEX stays high. In this case, unearned income will start hurting the FCF, instead of increasing it, and both accounts (CAPEX and decreasing unearned income) will lower the FCF. This is just speculation, but if this happens, it will also be a sign of Microsoft turning from an asset-light business to a lower-quality business.

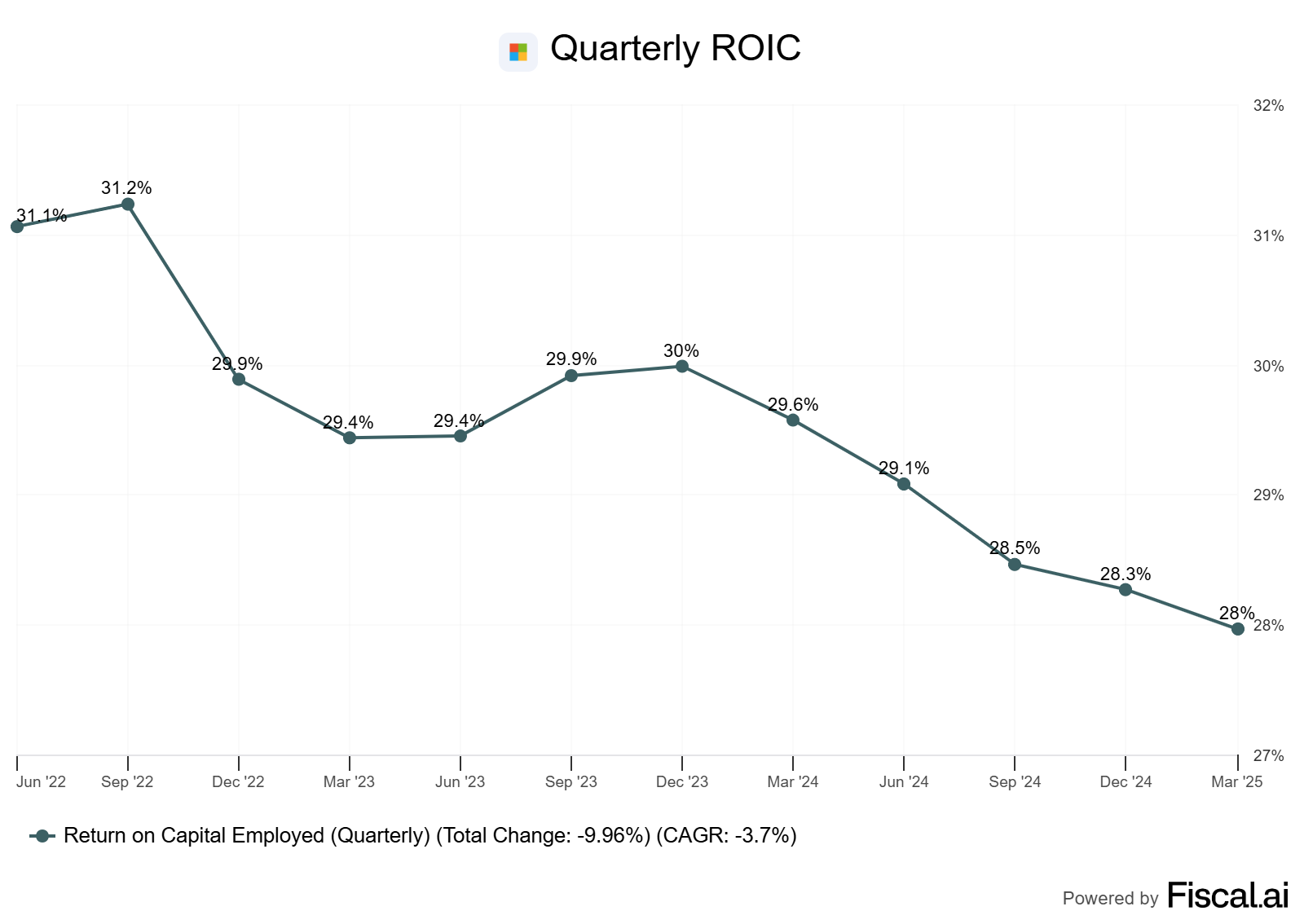

Return On Invested Capital:

Microsoft’s ROIC has consistently been high. This shows how strong the company is and has been for many years. However, there’s something worrying that favors the narrative of a worsening business: lower incremental ROIC.

As you can see, the company’s ROIC has been decreasing slowly during the past few years. This shows clearly that investments for the retained capital are not as profitable as they used to be. Of course, Microsoft is investing in future growth, but if these initiatives are not as profitable as the market expects, this can turn ugly rather quickly.

Again, nothing extraordinarily worrying, but lowering such a high ROIC means that the ROIC of current reinvestments is considerably lower than the current 28% ROIC (since new investments’ ROIC and old investments’ ROIC are averaged in the whole ROIC calculation).

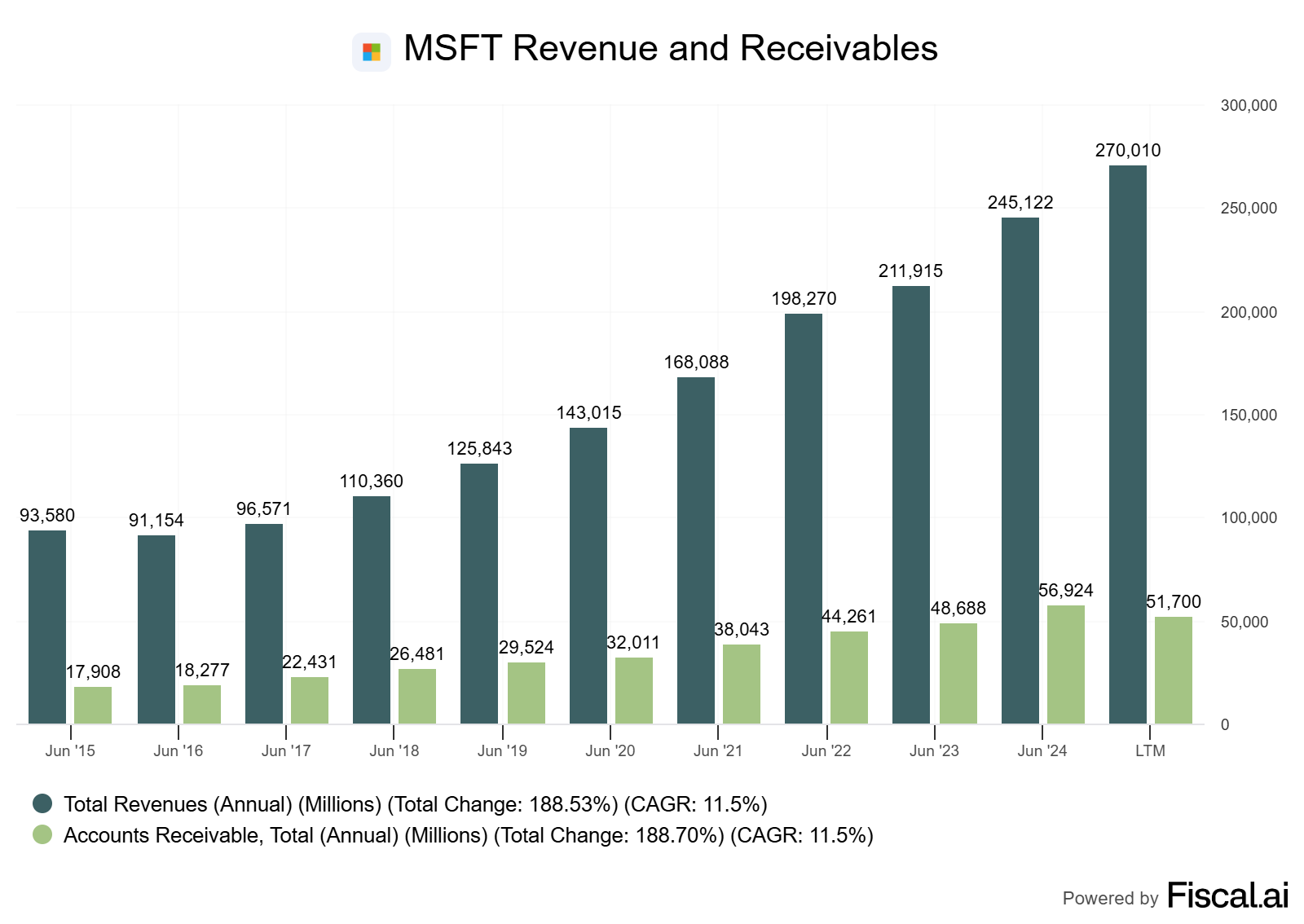

Receivables:

Revenue and receivables have usually grown together for Microsoft. As per the image below, both have grown 11.5% yearly since 2015.

However, this year, receivables have outpaced revenue growth significantly more than they used to. Revenue has grown $11.714 M, while receivables have grown $12.981 M. In the previous couple of years, the difference wasn’t more than a couple of hundred million.

Also, there’s a tendency in the company to increase receivables significantly at the end of the financial year, probably to push higher revenues for reporting purposes. This “over-recognition” is usually reversed in the first quarter of the following year. So the latest bump may be reversed.

Regardless, the incremental growth in receivables has consistently been at least over 2% higher, every quarter except in December 2024, than revenue growth.

My conclusion:

All of these red flags, individually, may not be a big thing. However, when you put them all together, the picture may be a little different. If I were an investor in Microsoft, which I’m not, I would be vigilant of the evolution of these metrics in the future.

Time will tell, but an aggressive accounting towards receivables accounts (overestimation of revenue), and a low incremental ROIC are not two good things to couple. Despite this, Microsoft remains one of the best businesses in the world.

Personally, I prefer avoiding Microsoft. These risks, plus the operational risk that every company faces, together with an eye-popping multiple on earnings of over 40 times earnings (over 50 times free cash flow), make me think that people are willing to pay too much for this good business. Probably, even disregarding the risks of the investment. Hence, unless the price goes down (considerably), I won’t buy Microsoft any time soon.