Does activity generate value?

An analysis of the portfolio

Active or passive. That’s a question that most people often ask. But we don’t read that often about studies to show if the activity has worked or not. For that reason, I’m comparing my portfolios at a given point in time to the current portfolio. Introducing the permanent portfolio.

The permanent portfolio is a screenshot of the portfolio I owned at a point in time. I will be studying the return of that untouched portfolio compared with the active portfolio I have managed. The idea comes from the annual investor meeting of Horos Asset Management, one of the best value funds in Spain. Without further ado, let’s dive in.

First of all, let’s start by saying that the portfolio has generated better results than the market, especially during the past 3 years. Out of 6 years, the portfolio has beaten the S&P 500 in 5 of them. Only in 2021 has the portfolio not returned more than the S&P 500. That means that for the past 4 years, in a row, the portfolio has outperformed, in some years widely, the return of the index.

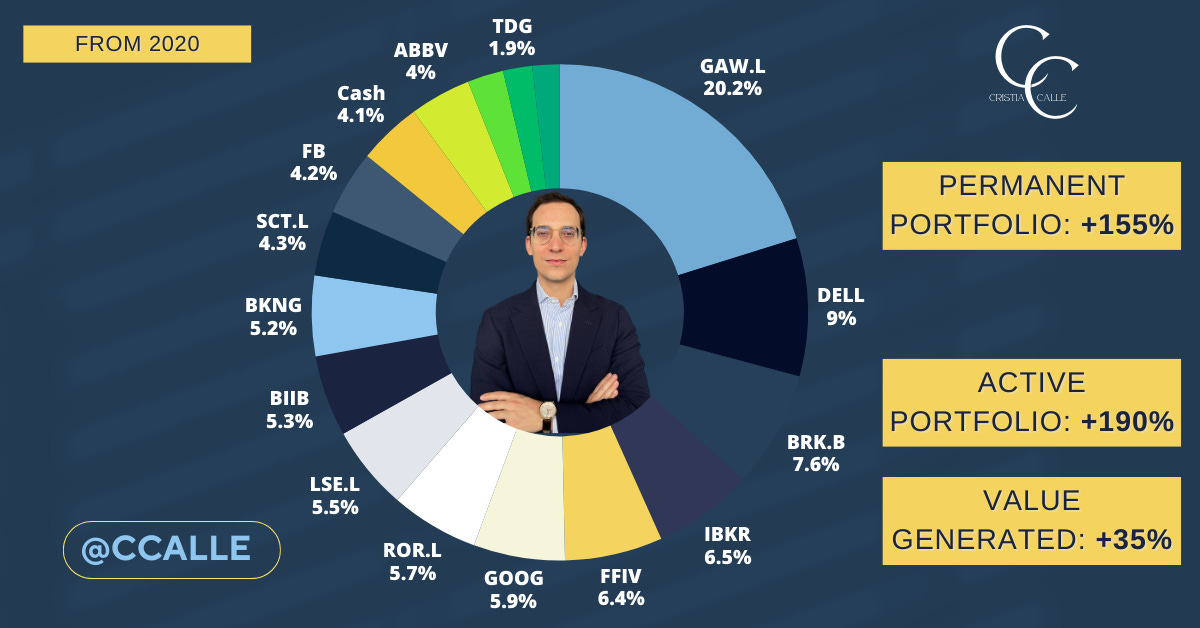

2020:

Hence, the portfolio has generated value for me and my copiers. But has activity generated value?

In 2020, the portfolio was heavily concentrated in stocks like Games Workshop (20% of the portfolio), DELL (9%), and Berkshire Hathaway (7%). There were some other quality names like Google, FFIV, and Facebook (now META), to name a few. This portfolio, untouched from 2020 to the 26th of November 2025, would have returned over 155%.

In the same period, the active portfolio, with the changes I make regularly in it, has returned over 190%, which is an excess return of 35%. To the question, has activity generated value? The answer is a clear yes.

But not only that: stock picking has also generated value, since the return of the permanent portfolio has also beaten the S&P 500.

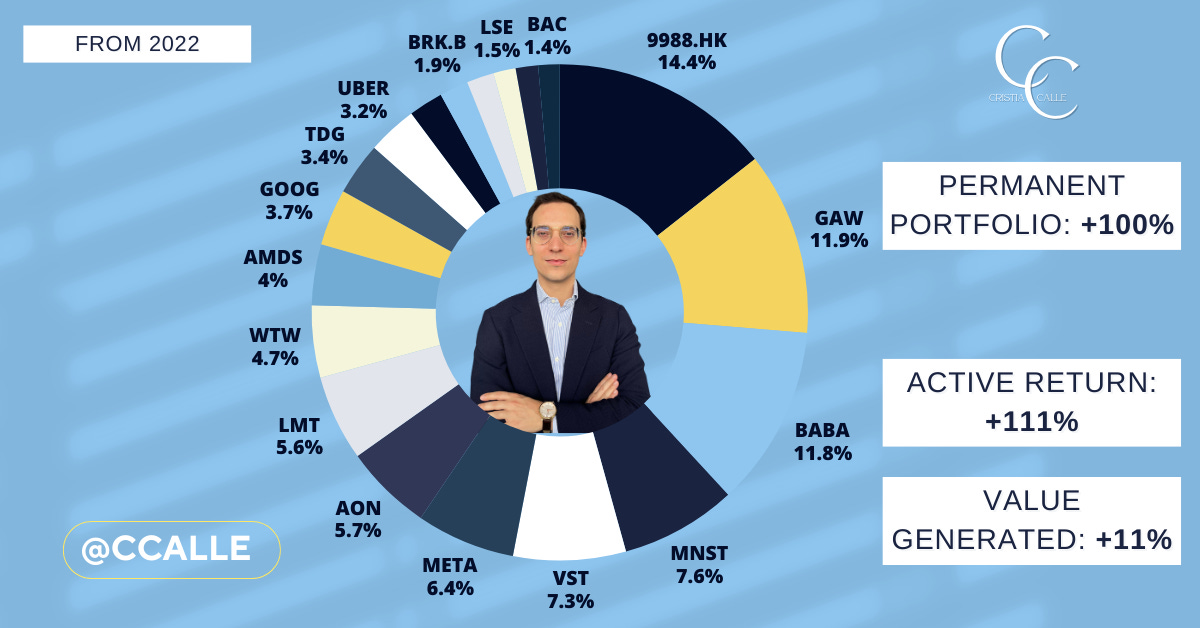

2022:

But I’d like to analyze the same for different periods. In this case, let’s analyze the portfolio from the start of 2022. I already had a big concentration in Alibaba, the main holding today, too. But I had already included names like Monster and Vistra.

In this scenario, the permanent portfolio returns over 100%, while the active portfolio has returned over 11%. Again, activity generates value.

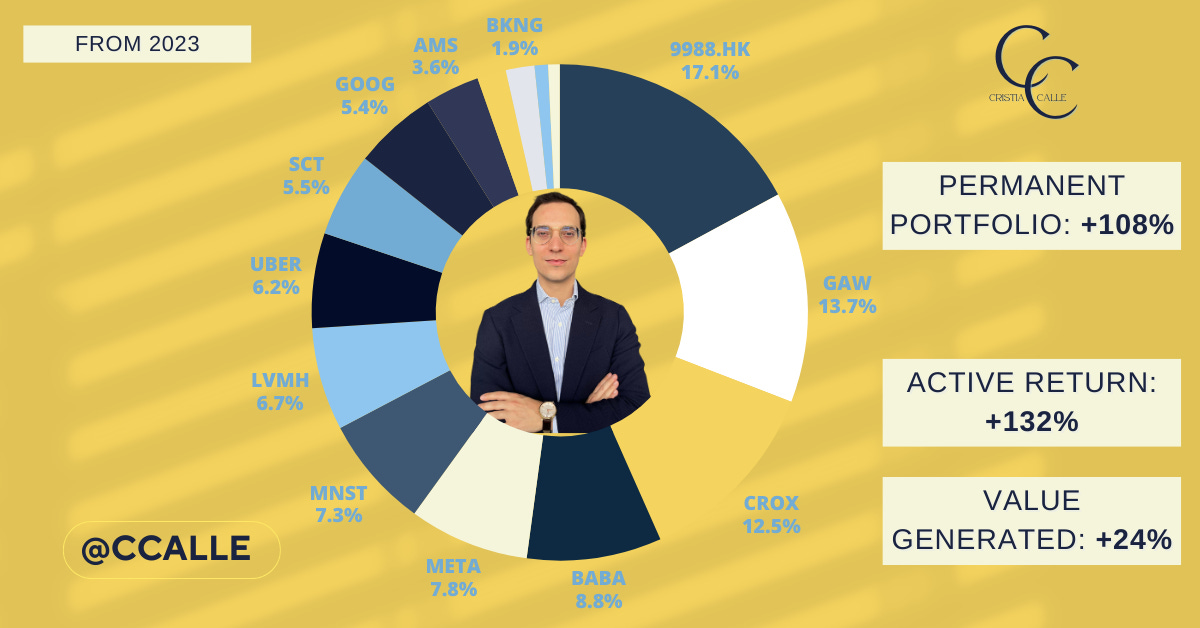

2023:

Now studying the permanent portfolio of 2023, which brought to the top holdings companies like Crocs, META, and LVMH, the return of the permanent portfolio was +108%, compared to +132% of the active portfolio. Once again, activity has generated value.

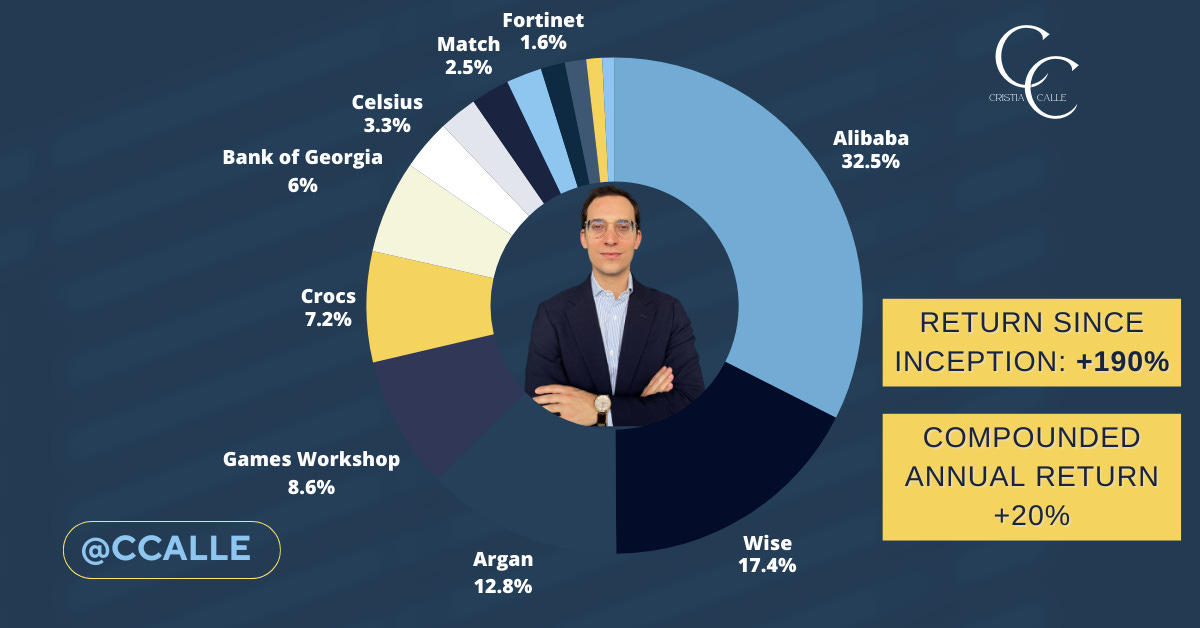

In summary, the portfolio has generated value through stock picking and through activity. The compounded annual return stays at over 20% per year, with a total return since inception of over 190%. But I wouldn’t like to finish the analysis here. Let me share with you some more insights:

Further considerations:

The active portfolio didn’t generate a lot of value compared to the permanent portfolio from 2022. And I wanted to analyze why that was happening.

One of the top holdings of 2022 was Vistra, which was acquired because the value of its assets was worth more than the value of its market cap. After obtaining a return of over 50%, I sold the shares.

However, the stock has jumped considerably since then, passing from trading at less than 1 times book value to over 21 times book value. The current PE ratio sits at above 60 times earnings. When I bought: less than 10. This stock, which has come to an unreasonable valuation by any means, has accounted for over 40% of the performance of the permanent portfolio.

This basically means that a stock that is probably in a frothy territory decreased the value added of activity.

And that’s OK with me. When I buy a business, I want to buy it for less than it is worth, and I’ll only sell it if someone is willing to pay me more for it than it is worth. Hence, I will lose any returns that may come from bubbles, but I will also not be exposed to bubbles when they occur. That’s a performance I’m willing to lose to avoid permanent losses of capital due to holding businesses for much more than they are worth.

Other than that, only META has had a contribution of over 30% of the total gains to a permanent portfolio: the permanent portfolio of 2023. However, it also had a huge impact on the active portfolio, since I took the weight of META to over 10% when it was widely understated by the market.

A call to caution:

I’ve also committed my share of mistakes during this time. Several of the companies I’ve bought not only haven’t generated returns that are better than the market’s, but also have generated negative results.

Biogen is the clearest example, which has generated a negative return of less than -20% for the permanent portfolio. This business actually generated a profit for the active portfolio, since I sold when their Alzheimer’s drug was approved, which was the peak of its valuation. However, the revenues of this drug are a lot less than I expected, which was a mistake. You can also make money even if you’re mistaken, but you need to learn not to commit that mistake again.

Amadeus has been another company that has returned -2% since I first bought it. The return for the active portfolio has, too, been low.

Finally, a mention of Crocs. At some point, its weight in the portfolio has been close to 10%. Since the start of 2023, the return of Crocs is almost -30%. However, the business is really cheap, and I think it will perform well in the future. As we’ve learned from Alibaba’s case, sometimes it takes a long time for the market to recognize the value of a business.

CCalle is a value investor and former CFO with more than 10 years of experience in finance. More than 2,300 people copy his investments with several million dollars of assets under copy.

You can visit his public portfolio here.

Learn more about CCalle here.